Defining the Scope and Eligibility of Wealth Management

In today’s intricate financial landscape, managing significant wealth involves more than just growing assets. It requires a sophisticated and holistic approach to safeguard, optimize, and strategically transfer your financial legacy. For individuals and families with substantial resources, Wealth Management offers a comprehensive framework designed to navigate complex financial challenges and achieve long-term aspirations.

We understand that true financial security extends beyond mere investment returns. It encompasses meticulous planning for taxes, estates, and even philanthropic endeavors, all while adapting to evolving market conditions and personal life changes. This guide aims to demystify Wealth Management, illustrating its core components, benefits, and how it differs from traditional financial planning.

Throughout this extensive guide, we will explore who typically benefits from these specialized services, the essential qualifications to look for in a wealth manager, and the critical role it plays in intergenerational wealth transfer. We will also examine how the industry is evolving, from digital advancements to the impact of major demographic shifts, providing you with the insights needed to make informed decisions for your financial future.

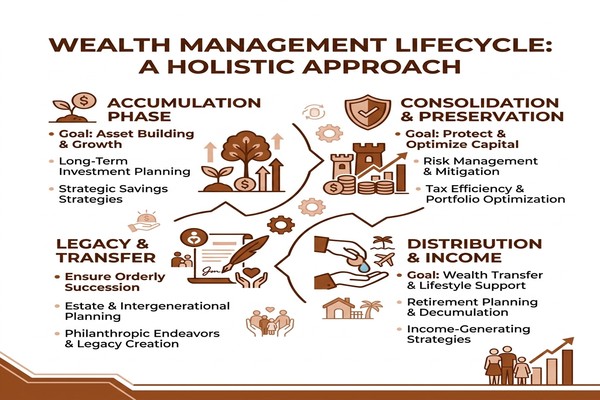

Wealth management stands as a specialized discipline within financial services, tailored to meet the multifaceted needs of affluent individuals, families, and even institutions. At its heart, it’s about providing a comprehensive, integrated approach to managing a client’s entire financial picture, going far beyond basic investment advice. It encompasses a wide array of services designed to grow, preserve, and protect wealth, ensuring its efficient transfer across generations.

Unlike general financial planning, which often focuses on specific financial goals like retirement or college savings for a broader audience, wealth management caters to those with substantial liquid assets. These clients typically have complex financial situations that necessitate a coordinated strategy involving investment management, tax planning, estate planning, and more. It’s about creating a personalized roadmap that aligns financial decisions with life goals, spending patterns, and long-term legacy aspirations. This holistic perspective is crucial for individuals who are not just accumulating wealth but actively managing and planning for its future. For those exploring diverse investment avenues, including non-traditional assets, understanding the nuances of how these fit into a broader strategy is key. For example, some individuals might be interested in exploring new frontiers such as Alternative wealth management options that deviate from conventional stocks and bonds.

Distinguishing Individual from Institutional Investing

While the principles of sound investing often apply universally, there are fundamental differences between individual and institutional investing that wealth management addresses.

One primary distinction lies in time horizons. Institutions, such as pension funds or endowments, often operate with perpetual or very long timeframes, allowing them to ride out market fluctuations and focus on long-term growth without immediate liquidity concerns. Individual investors, however, face finite life horizons. This necessitates strategies that account for both the accumulation of wealth during working years and its decumulation during retirement, including planning for asset transfer at the end of life. These strategies must navigate varying laws and regulations governing inheritance and estate distribution.

Another significant difference is tax implications. Individual investors are subject to a complex web of locality-based taxes on investment returns, which can vary significantly depending on residency and the type of asset. Wealth managers employ sophisticated portfolio investment techniques aimed at optimizing after-tax returns, a consideration that is often less prominent for tax-exempt institutions. We focus on ensuring that our clients’ portfolios are structured not just for growth, but also for tax efficiency, maximizing the net benefit of their investments.

Common Eligibility Thresholds and Client Profiles

Wealth management services are typically geared towards individuals and families who have accumulated a certain level of investable assets. While there isn’t a universally fixed minimum, a common threshold often cited for engaging comprehensive wealth management services is around $1 million in liquid assets. This level of wealth usually indicates a financial situation complex enough to benefit from an integrated approach.

However, the industry also segments clients into different tiers:

- Mass Affluent: Generally individuals with $100,000 to $1 million in investable assets. They might access guided advice or dedicated advisors, with services becoming more personalized at higher asset levels.

- High-Net-Worth (HNW) Individuals: Typically defined as those with $1 million to $5 million (or sometimes up to $10 million) in investable assets. These clients receive a broader range of services, including advanced tax and estate planning.

- Ultra-High-Net-Worth (UHNW) Individuals: Clients with $10 million or more in investable assets. This group often qualifies for exclusive services like private banking and family offices, which offer highly customized solutions, sometimes extending to non-financial aspects of their lives.

For instance, some large financial institutions differentiate their services, offering “Global Wealth Management” for accounts below a certain threshold (e.g., $10 million) and “Private Wealth Management” for those with significantly higher assets (e.g., over $20 million). These distinctions reflect the increasing complexity and customization required as wealth levels grow. Family offices, whether single or multi-family, represent the pinnacle of personalized wealth management, offering comprehensive oversight for the most affluent families.

Core Pillars of a Comprehensive Wealth Management Strategy

A robust wealth management strategy is built upon several interconnected pillars, each designed to contribute to the client’s overall financial well-being and long-term objectives. It’s a dynamic process that adapts to market changes, life events, and evolving financial goals, ensuring that wealth is not just accumulated but also preserved and strategically utilized.

At the foundation is risk management, which involves identifying, assessing, and mitigating potential financial threats. This goes hand-in-hand with asset allocation, the process of distributing investments across various asset classes (stocks, bonds, real estate, commodities, etc.) to balance risk and reward. Diversification further refines this by spreading investments within each asset class to reduce exposure to any single security or sector. The principles of Modern Portfolio Theory often guide these decisions, suggesting that a diversified portfolio can lead to more predictable returns, especially when supported by prudent market regulation. We believe in crafting portfolios that are not only aligned with an individual’s risk tolerance but also resilient enough to withstand market volatility.

Tax Optimization and Estate Planning

One of the most critical components of wealth management is tax optimization. This involves employing various strategies to minimize tax liabilities across investments, income, and wealth transfer. Tax-smart techniques are applied throughout the year to managed portfolios, aiming to reduce the overall tax impact on earnings. This proactive approach helps clients retain a larger portion of their wealth, contributing significantly to long-term growth.

Beyond investment taxes, wealth management delves deep into estate planning. This crucial area focuses on the efficient and tax-effective transfer of assets to beneficiaries, aligning with the client’s wishes and minimizing potential disputes. Strategies often include:

- Gift Tax Exclusions: Utilizing annual and lifetime gift tax exemptions to transfer wealth during one’s lifetime, reducing the size of the taxable estate. For example, in 2024, individuals can gift up to $18,000 per recipient annually without incurring gift tax.

- Irrevocable Trusts: Establishing trusts to remove assets from the taxable estate, protect them from creditors, and ensure they are distributed according to specific instructions.

- Succession Planning: For business owners, this involves creating a clear roadmap for the transfer of business ownership and management, ensuring continuity and preserving value.

- Intergenerational Wealth Transfer: Developing strategies to educate heirs and prepare them for responsible stewardship of inherited wealth, often involving family governance structures.

The landscape of tax regulations is constantly shifting, making specialized expertise invaluable. For instance, the impending sunset of certain Tax Cuts and Jobs Act (TCJA) provisions in 2026 could significantly impact estate and gift tax exemptions. Navigating such changes, or even dealing with complex situations like Wealth-related ERC audits, requires a deep understanding of tax law and proactive planning. We work closely with tax and legal specialists to ensure our clients’ plans are robust and compliant.

Philanthropy and Family Governance

Wealth management extends beyond personal financial gain to encompass broader societal impact and family legacy. Philanthropy is an increasingly important aspect for many affluent individuals and families. Wealth managers assist in structuring charitable giving strategies that align with a client’s values, maximize their impact, and offer tax advantages. This can involve setting up donor-advised funds, private foundations, or integrating social finance investments into their portfolio to achieve both financial returns and philanthropic goals.

Family governance focuses on establishing structures and processes to manage family wealth, businesses, and relationships across generations. This includes:

- Aligning Family Values: Helping families articulate their shared values and mission statements regarding wealth.

- Educational Programs for Heirs: Preparing younger generations for the responsibilities of wealth stewardship, often through financial literacy programs and mentorship.

- Legacy Preservation: Ensuring that the family’s values, traditions, and philanthropic endeavors endure for future generations.

These elements collectively ensure that wealth serves not just as a financial asset, but as a tool for achieving personal fulfillment, societal good, and a lasting family legacy.

Navigating Professional Qualifications and Fee Structures

Choosing the right wealth manager is a critical decision that can significantly impact your financial future. It’s essential to understand the qualifications, ethical obligations, and fee structures that define the professionals in this field.

Credentials and Fiduciary Standards

A reputable wealth manager will hold specific credentials that demonstrate their expertise and commitment to professional standards. Look for certifications such as:

- Certified Financial Planner (CFP®): Signifies competence in financial planning, including investments, insurance, retirement, and estate planning.

- Chartered Financial Analyst (CFA®): Highly respected in the investment management industry, indicating expertise in investment analysis and portfolio management.

- Certified Private Wealth Advisor (CPWA®): Focuses specifically on the unique needs of high-net-worth individuals, covering advanced wealth management strategies.

Beyond credentials, it’s paramount to work with a wealth manager who adheres to a fiduciary standard. A fiduciary is legally and ethically bound to act in their clients’ best interests, placing those interests above their own. This contrasts with a suitability standard, where an advisor only needs to recommend products that are “suitable” for a client, even if better options exist. We firmly believe in upholding the fiduciary standard, ensuring our advice is always aligned with your objectives.

You can verify an advisor’s credentials and check for any disciplinary actions through regulatory bodies like the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Authority (FINRA). These resources provide transparency and help ensure you are working with a qualified and ethical professional.

Fee Structures

Wealth management services come with various fee structures, and understanding them is key to evaluating costs and value. The most common models include:

- Assets Under Management (AUM) Fee: This is the most prevalent model, where the advisor charges a percentage of the total assets they manage for you. The median advisory fee for up to $1 million AUM is around 1%, but this percentage often decreases as the AUM increases, reflecting economies of scale.

- Fee-Only: Advisors charge a flat fee, an hourly rate, or a retainer for their services, regardless of the products they recommend or the assets managed. This model is often preferred by those seeking unbiased advice, as it removes any potential conflicts of interest related to commissions.

- Commission-Based: Advisors earn commissions from the financial products they sell, such as insurance policies, mutual funds, or annuities. While this can result in no direct out-of-pocket fees, it can create conflicts of interest.

- Fee-Based: A hybrid model where advisors earn both AUM fees or flat fees AND commissions from product sales.

We prioritize transparency in our fee structures, ensuring clients fully understand how they are charged and the value they receive for those fees. It’s crucial to discuss and clarify all potential costs upfront, including any underlying expenses from brokerage, funds, or trading.

When to Engage Professional Wealth Management Services

Deciding when to engage a wealth manager is a personal choice, but several indicators suggest it might be the right time:

- Complex Financial Situations: When your financial life becomes intricate, perhaps involving multiple investment accounts, real estate holdings, business interests, or international assets, a wealth manager can provide the necessary coordination and expertise.

- Significant Life Transitions: Major life events such as starting a business, selling a company, receiving a large inheritance, getting married, divorcing, or nearing retirement often create new financial complexities that benefit from professional guidance.

- Lack of Time or Expertise: If you find yourself overwhelmed by managing your finances, lack the time to stay abreast of market changes and tax laws, or simply prefer to delegate these responsibilities to an expert, a wealth manager can provide immense value.

- Specific Asset Thresholds: While not a strict rule, having investable assets typically exceeding $100,000 to $1 million often makes comprehensive wealth management a cost-effective and beneficial option.

- Desire for Holistic Planning: If you’re looking for more than just investment advice-seeking guidance on tax planning, estate planning, risk management, and philanthropic strategies-a wealth manager offers that integrated approach.

- Planning for Intergenerational Wealth Transfer: When the goal is not just to grow your wealth but also to ensure its smooth and tax-efficient transfer to future generations, a wealth manager’s expertise in estate and succession planning becomes indispensable.

The right time is when you recognize the need for a strategic partner to help you navigate your financial journey, optimize your wealth, and secure your legacy.

The Future of Wealth: AI, Digital Assets, and the Great Wealth Transfer

The wealth management industry is in a constant state of evolution, driven by technological advancements, shifting demographics, and changing client expectations. Understanding these trends is crucial for both wealth managers and clients seeking to future-proof their financial strategies.

One of the most impactful demographic shifts is the Great Wealth Transfer, where an unprecedented amount of wealth is expected to pass from older generations to younger ones. This transfer brings with it new challenges and opportunities, as younger heirs may have different financial priorities, values, and technological preferences. Coupled with increasing market volatility and the growing importance of behavioral finance, wealth managers are adapting their approaches to provide more personalized, values-driven advice. Risk mitigation strategies are also evolving to address these new dynamics.

The Role of Technology in Modern Wealth Management

Technology is rapidly reshaping how wealth management services are delivered and experienced.

- Artificial Intelligence (AI): AI is transforming various aspects of wealth management, from automating routine tasks and data analysis to providing personalized investment insights. AI-powered tools can help advisors identify trends, optimize portfolios, and even predict client needs. Firms are seeing significant efficiency gains, with some reporting saving hundreds of hours per month through AI implementation. However, building trust in AI is paramount, requiring robust governance, oversight, and data security measures.

- Robo-Advisors: These automated platforms offer algorithm-driven financial planning services with little to no human supervision. They provide a lower-cost alternative for investors, particularly those with smaller portfolios, and have pushed the industry towards greater accessibility and efficiency.

- Digital Tools and Platforms: Online portals, mobile apps, and digital dashboards provide clients with real-time access to their portfolios, performance reports, and financial plans. These tools enhance transparency and communication, empowering clients to stay informed and engaged.

- Data Security: With increased digitalization comes a heightened focus on cybersecurity. Protecting sensitive client data from breaches and fraud is a top priority, and advanced security protocols are integral to modern wealth management operations.

- Automated Rebalancing: Technology enables automated rebalancing of portfolios, ensuring they stay aligned with target asset allocations without constant manual intervention.

- Digital Assets: The emergence of cryptocurrencies and other digital assets presents both opportunities and complexities for wealth managers. Integrating these assets into a holistic wealth management strategy requires specialized knowledge and secure platforms. For those looking to manage their digital holdings responsibly, seeking guidance on Safe Bitcoin Wealth Management and other cryptocurrencies is becoming increasingly relevant.

These technological advancements are creating “shadow efficiencies,” allowing advisors to serve clients more effectively without necessarily altering client-advisor ratios.

Evolving Service Models and Private Banking

The traditional models of wealth management are also evolving to meet diverse client needs:

- Private Banking: Historically the domain of the ultra-wealthy, private banking continues to offer exclusive services, including personalized lending, trust services, and access to unique investment opportunities.

- Multi-Family Offices: Building on the single-family office model, these firms provide comprehensive wealth management services to several affluent families, leveraging shared resources and expertise. They often offer a wide range of services, from investment management and tax planning to concierge services and family education.

- Boutique Advisory Firms: These independent firms often specialize in specific niches or offer highly personalized services, appealing to clients who prefer a more tailored and less institutional approach.

- Hybrid Digital-Human Models: Many firms are adopting a hybrid approach, combining the efficiency of digital tools and robo-advisors with the personalized guidance of human advisors. This allows for scalability while maintaining a high level of client service.

- Concierge Services: For UHNW clients, wealth management sometimes extends to non-financial services, including budgeting, education planning for children, household management, and travel arrangements, reflecting a “financial life management” approach.

- Global Wealth Trends: The industry is also responding to global trends, such as the increasing interconnectedness of economies and the need for cross-border wealth management solutions for international clients.

The evolution of these service models underscores a shift towards a more client-centric approach, where flexibility, personalization, and comprehensive support are paramount.

Frequently Asked Questions about Wealth Management

Here, we address some common questions to further clarify the role and benefits of wealth management.

How does wealth management differ from standard financial planning?

While both aim to help individuals achieve financial goals, wealth management is a more comprehensive and integrated service typically geared towards high-net-worth (HNW) and ultra-high-net-worth (UHNW) individuals and families. Standard financial planning often focuses on specific goals like retirement, budgeting, or college savings for a broader audience. Wealth management, however, encompasses a wider array of services, including sophisticated investment management, advanced tax planning, estate planning, philanthropic strategies, and even family governance, all coordinated into a single, holistic strategy. It’s about managing the entire financial ecosystem of a complex client.

What are the typical fees associated with high-net-worth advisory services?

The most common fee structure for high-net-worth advisory services is a percentage of Assets Under Management (AUM). This typically ranges from around 0.5% to 1.5% annually, with the percentage often decreasing as the total AUM increases. For example, a client with $1 million might pay 1%, while a client with $10 million might pay 0.75%. Other fee structures include flat fees, hourly rates, or retainer fees, especially for specific projects or for services that don’t involve managing assets. Some advisors operate on a commission-based or fee-based (hybrid) model, which can introduce potential conflicts of interest, hence the preference for fee-only or AUM-based fiduciaries. We always ensure full transparency regarding our fee structure and the value we provide.

What role does a wealth manager play in estate and succession planning?

A wealth manager plays a pivotal role in estate and succession planning by integrating these critical components into the overall financial strategy. For estate planning, they work with legal experts to help clients structure their assets for tax-efficient transfer to beneficiaries, minimizing estate and gift taxes. This involves advising on the use of wills, trusts (such as irrevocable or revocable trusts), and charitable giving vehicles. For business owners, wealth managers facilitate succession planning, ensuring a smooth transition of leadership and ownership, whether to family members, employees, or external buyers. They help value the business, identify potential successors, and create strategies to preserve the business’s value and provide for the owner’s retirement. Their role is to ensure that the client’s legacy and wishes are honored while navigating complex legal and tax landscapes.

Conclusion

In an increasingly complex financial world, effective wealth management is not a luxury but a necessity for individuals and families with substantial assets. It offers more than just financial advice; it provides a pathway to financial clarity, peace of mind, and strategic growth. By adopting a holistic approach that integrates investment management, tax optimization, estate planning, and philanthropic strategies, wealth management helps clients navigate challenges, capitalize on opportunities, and adapt to life’s ever-changing landscape.

We are committed to providing comprehensive, personalized solutions that go beyond traditional investment services. Our goal is to offer holistic oversight that ensures your wealth is not only preserved and grown but also aligned with your deepest values and aspirations. By understanding the nuances of your financial situation and anticipating future trends, we help in future-proofing wealth and securing a sustainable legacy for generations to come. The journey of wealth is continuous, and with the right strategic partner, you can confidently build, protect, and transfer your financial future.