Why Insurance is a Pillar of Personal Finance and Insurance

Life is full of unexpected turns, and many of them come with significant financial consequences. Building a strong personal financial foundation means being ready for these moments. It’s about more than just managing your daily money; it’s about creating lasting security for yourself and your loved ones.

We often focus on saving and investing for our future goals. However, insurance is an equally critical part of this picture. It acts as a powerful shield, offering vital risk mitigation and helping with wealth preservation. Think of how essential good health coverage can be when unexpected medical costs suddenly arise.

In this extensive guide, we will explore why insurance is a central pillar of comprehensive financial planning. We will delve into various types of coverage, including essential health protection. Our goal is to help you understand how to protect against financial risks, assess your unique needs, and build true crisis preparedness for a more secure future.

Insurance is often mistakenly viewed as a mere expense, but in reality, it’s a foundational component of a robust financial strategy. Its primary role is risk transfer. Instead of shouldering the full financial burden of an unexpected event yourself, you transfer that risk to an insurer by paying regular premiums. This simple mechanism brings profound benefits to your personal finance journey.

This risk transfer provides financial predictability. When you have appropriate coverage, you know that certain catastrophic events, like a major illness, a car accident, or damage to your home, won’t completely derail your financial plans. This predictability allows you to confidently pursue other financial goals, knowing there’s a safety net in place. Without insurance, an unforeseen event could lead to significant debt, forcing you to deplete savings, sell assets, or even declare bankruptcy. Medical bills, for instance, are a leading cause of debt among those without adequate health insurance coverage.

Insurance also plays a crucial role in debt prevention and capital preservation. Imagine years of diligently saving for a down payment on a home or building a retirement fund. A sudden, uninsured event could wipe out those hard-earned assets in an instant. Insurance protects your existing capital and prevents you from incurring new, often overwhelming, debt. It means that your wealth, whether in the form of savings, investments, or property, is safeguarded against unexpected losses. For more in-depth guidance and expert perspectives on managing your finances and understanding the role of protection, exploring resources that offer comprehensive Personal finance and insurance advice can be incredibly beneficial.

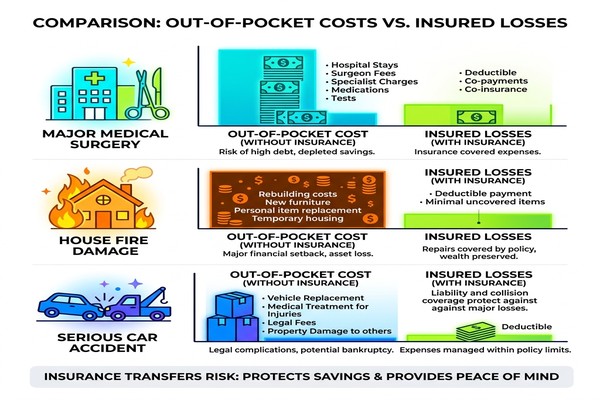

To illustrate the impact, consider the potential out-of-pocket costs versus insured losses for common events:

This table clearly demonstrates how a relatively small premium payment can protect you from potentially devastating financial losses, enabling true asset protection and peace of mind.

Essential Coverage Types for Every Life Stage

As your life evolves, so do your financial risks and insurance needs. While the specifics may vary, certain types of insurance are universally important at various stages, forming a critical protective layer for your financial well-being.

Health Insurance

Perhaps one of the most critical forms of protection, health insurance guards against the high costs of medical care. From routine check-ups to emergency surgeries and chronic disease management, healthcare expenses can quickly accumulate to tens or even hundreds of thousands of dollars. Without health insurance, these costs can be financially crippling, often leading to significant medical debt. It’s a cornerstone of financial planning, ensuring you can access necessary care without sacrificing your financial stability. Understanding your options and navigating the complexities of healthcare coverage is vital for sound Health insurance personal finance.

Property and Casualty Insurance

This category includes policies that protect your tangible assets and shield you from liability.

- Homeowners Insurance: For homeowners, this policy protects your dwelling and personal belongings against perils like fire, theft, and natural disasters. It also typically includes liability coverage, protecting you if someone is injured on your property.

- Renters Insurance: If you rent, this policy protects your personal possessions and provides liability coverage, often for a very affordable premium.

- Auto Insurance: Required in most states, auto insurance covers damage to your vehicle, damage to other vehicles, and liability for injuries or property damage you cause in an accident. It’s essential for protecting your driving privileges and financial assets.

Umbrella Liability Insurance

This type of policy provides an extra layer of liability coverage beyond what your homeowners and auto policies offer. If you face a lawsuit that exceeds the limits of your primary policies, an umbrella policy kicks in to cover the difference, protecting your assets from being seized. It’s particularly valuable for individuals with significant assets or those who face higher liability risks.

Long-Term Care Insurance

As we age, the likelihood of needing assistance with daily activities increases. Long-term care insurance helps cover the costs of services like nursing home care, assisted living facilities, or in-home care, which are typically not covered by standard health insurance or Medicare. Without it, the significant costs of long-term care can quickly deplete retirement savings.

Protecting Your Earning Power with Personal Finance and Insurance

While many focus on life insurance, the statistics tell a compelling story about the often-overlooked need for disability insurance. You are statistically more likely to become disabled and unable to work than to die prematurely. Disability insurance provides income replacement if you become ill or injured and cannot perform your job. This coverage is absolutely critical, especially during your peak earning years when your income supports your household, mortgage, and other financial obligations.

Common disability triggers can range from accidents and injuries to serious illnesses like cancer, heart disease, or chronic conditions that prevent you from working. Both short-term and long-term disability policies exist. Short-term typically covers a few months, while long-term can provide benefits for several years or until retirement age. Relying solely on employer-provided disability insurance can be risky, as these policies often have benefit caps and may only cover a portion of your income, leaving high earners particularly vulnerable. Supplementing with an individual policy can ensure adequate protection.

Building a Legacy through Personal Finance and Insurance

Life insurance is a cornerstone of financial planning for anyone with dependents or financial obligations they wish to protect. Its primary purpose is to provide financial security for your loved ones after your passing. The death benefit, typically paid out tax-free to beneficiaries, can be used for a variety of purposes:

- Income Replacement: To replace your lost income, allowing your family to maintain their standard of living.

- Debt Repayment: To pay off mortgages, car loans, or other debts, preventing financial strain on your survivors.

- Future Expenses: To cover future costs like college tuition for children or funeral expenses.

- Estate Liquidity: For larger estates, it can provide funds to cover estate taxes or other settlement costs without having to sell off assets.

There are two main types of life insurance:

- Term Life Insurance: Provides coverage for a specific period (e.g., 10, 20, or 30 years). It’s generally more affordable and is ideal for covering financial obligations that will eventually end, such as a mortgage or child-rearing years.

- Whole Life Insurance (and other permanent policies like Universal Life): Offers lifelong coverage and typically includes a cash value component that grows over time on a tax-deferred basis. This cash value can be borrowed against or withdrawn, providing a living benefit.

Beyond pure protection, some life insurance policies can offer tax advantages. The death benefit is typically tax-free for beneficiaries. In some jurisdictions, certain premiums may offer tax deductions (e.g., under Section 80C or 80D for health-related components in some countries), and the cash value growth in permanent policies is tax-deferred. This makes life insurance a powerful tool for wealth transfer and legacy building, ensuring your financial wishes are met even after you’re gone.

Assessing Your Needs and Identifying Coverage Gaps

Understanding your personal insurance needs is not a one-size-fits-all endeavor; it requires a thoughtful assessment of your unique circumstances. Your life stage, family situation, income, debts, and assets all play a crucial role in determining the right types and amounts of coverage.

Start by evaluating your current life stage:

- Young Single Professional: Focus on health, auto, and disability insurance to protect your income and health.

- Growing Family: Life insurance becomes paramount to protect dependents, along with robust health, homeowners, and disability coverage.

- Mid-Career with Assets: Consider umbrella liability, long-term care, and potentially adjusting life insurance as debts decrease and assets grow.

- Approaching/In Retirement: Long-term care insurance is often a priority, while life insurance might shift to estate planning or legacy purposes.

Next, analyze your income-to-debt ratio and asset evaluation. How much income do you need to replace if you can’t work? How much debt would your family inherit if you passed away? What is the value of your home, cars, and other significant assets that need protection? These questions help quantify your coverage needs.

A common challenge is identifying coverage gaps. Many individuals are under-insured, meaning their current policies wouldn’t adequately cover the financial impact of an unforeseen event. For example, employer-provided life and disability insurance, while beneficial, often has limitations. Employer policies may only cover a fraction of your income, and they are typically tied to your employment, meaning they could be lost upon a job change. This makes supplemental policies crucial for consistent protection. We believe in nurturing financial well-being, much like tending to an Office plant financial growth – consistent care and attention lead to robust results.

Conversely, some might be over-insured, paying for coverage they no longer need or that is excessive for their current risk profile. Regularly reviewing your policies helps you strike the right balance, ensuring you’re not paying for unnecessary protection while also avoiding critical vulnerabilities. For instance, if your mortgage is paid off and your children are financially independent, you might reduce your life insurance coverage.

Best practices suggest that an annual review of your insurance portfolio, along with reassessments after major life events, is essential. This helps ensure your policies remain aligned with your evolving needs, offering the right level of protection without being a financial drain.

Integrating Insurance into a Holistic Financial Strategy

Insurance is not a standalone product; it’s an integral component that weaves into the fabric of your entire financial strategy. A holistic approach means viewing insurance alongside your savings, investments, retirement plans, and estate planning, ensuring all elements work in harmony to achieve your long-term goals.

Annual Policy Reviews and Life Event Triggers: Your insurance needs are dynamic, changing with every significant life event. Marriage, the birth of a child, purchasing a home, starting a business, a significant career change, or even a change in health status should all trigger a review of your policies. An annual financial check-up is also a prime opportunity to assess if your coverage still aligns with your current situation and future aspirations. This proactive approach helps prevent being under-insured as your responsibilities grow or over-insured as they diminish.

Employer Benefit Optimization: Many professionals have access to group insurance through their employers, which can account for a significant portion of their total compensation. However, statistics show that many utilize only a fraction of what’s offered or don’t fully understand its limitations. It’s crucial to understand the specifics of your employer-provided life, health, and disability insurance. Identify any gaps, such as benefit caps or lack of portability, and consider supplementing with individual policies to ensure comprehensive protection that isn’t tied to your job.

Tax-Advantaged Savings and HSA Integration: Insurance can also integrate with tax-advantaged savings vehicles. For example, Health Savings Accounts (HSAs) are powerful tools for medical expenses when paired with high-deductible health plans. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. This triple-tax advantage makes HSAs an excellent way to save for future healthcare costs, effectively combining health insurance with a long-term savings strategy. Similarly, robust insurance coverage frees up more capital to contribute to retirement accounts like 401(k)s. Statistics show that 401(k) savers hold 29% more retirement funds than nonparticipants, underscoring the power of consistent saving, which insurance helps protect.

The Role of a Financial Advisor: Navigating the complexities of insurance and integrating it into your overall financial strategy can be challenging. This is where a qualified financial advisor plays a crucial role. An advisor can:

- Assess Your Needs: Help you objectively evaluate your life stage, risk tolerance, and financial goals to determine appropriate coverage.

- Identify Gaps: Pinpoint areas where you might be under-insured or have insufficient coverage.

- Optimize Policies: Suggest how to best combine employer benefits with individual policies.

- Integrate with Overall Plan: Ensure your insurance strategy complements your investment, retirement, and estate plans.

- Provide Objective Advice: Offer unbiased recommendations, helping you understand the nuances of different policy types and providers.

By working with an advisor, you gain a clearer understanding of how insurance acts as a protective layer, allowing your other financial assets to grow and your long-term plans to unfold securely.

Frequently Asked Questions about Personal Finance and Insurance

How do I determine if I am under-insured or over-insured?

Determining if you are under-insured or over-insured involves a comprehensive review of your current financial situation and policies.

- Under-insured: You are likely under-insured if a major event (e.g., severe illness, death of a breadwinner, significant property damage) would cause severe financial hardship, deplete your savings, or force you into substantial debt. This often happens when coverage limits are too low, or you’ve neglected certain types of insurance (like disability or umbrella liability). A debt-to-income analysis can reveal vulnerabilities; if your income suddenly stopped, how long could your savings cover your expenses and debts?

- Over-insured: You might be over-insured if you’re paying for coverage you no longer need, or if the cost of premiums outweighs the potential financial loss. For example, maintaining a large life insurance policy after your children are grown and your mortgage is paid off, or having duplicate coverages. Regular annual reviews are key to assessing if your coverage levels align with your current assets, liabilities, and family responsibilities.

Why should I supplement my employer-provided disability insurance?

Employer-provided disability insurance is a valuable benefit, but it often has limitations that can leave you vulnerable, especially if you are a high earner.

- Benefit Caps: Group policies often cap the monthly payout, which might only cover a fraction of your actual income, particularly for higher-income professionals.

- Portability Issues: Employer coverage is typically tied to your job. If you change employers or lose your job, you often lose this coverage, leaving you exposed during transition periods.

- Definition of Disability: Group policies may have a more restrictive definition of “disability,” making it harder to qualify for benefits compared to individual policies.

- Taxation: Employer-paid premiums often mean that disability benefits, if received, are taxable, further reducing your net income replacement. Supplementing with an individual disability income policy allows you to secure higher coverage limits, ensure portability, and often benefit from a broader definition of disability, providing more robust and consistent protection regardless of your employment status.

When is the best time to review my insurance policies?

Your insurance needs are not static; they evolve with your life. Therefore, regular reviews are crucial. The best times to review your insurance policies include:

- Major Life Events:Marriage or Divorce: Changes in dependents, beneficiaries, and shared assets.

- Birth or Adoption of a Child: Increased need for life insurance and potentially health coverage for the new family member.

- Purchasing a Home: Requires homeowners insurance and often increased life insurance to cover the mortgage.

- Significant Career Change or Promotion: Impacts income replacement needs for disability and life insurance.

- Children Becoming Financially Independent: May allow for a reduction in life insurance coverage.

- Retirement: Focus shifts to long-term care, and life insurance may transition to estate planning.

- Annually: A yearly financial check-up is an excellent opportunity to review all your policies. This ensures your coverage amounts are still appropriate, premiums are competitive, and beneficiaries are up to date. It also helps you identify any new risks or changes in your financial situation that warrant adjustments.

Conclusion

In the intricate landscape of personal finance, insurance stands as a vital, often underestimated, pillar. It’s more than just a financial product; it’s a strategic tool for proactive risk management, offering a crucial layer of protection against life’s unpredictable events. By understanding the various types of coverage, assessing your unique needs, and integrating insurance into your broader financial strategy, you can cultivate long-term security and achieve genuine financial peace of mind.

Embracing a holistic view of your finances, where insurance complements your savings, investments, and retirement plans, allows you to future-proof your assets and build a resilient financial foundation. Don’t leave your future to chance; take deliberate steps to secure it with the right personal finance and insurance solutions.