Deconstructing the 12-Month Cash Flow Statement

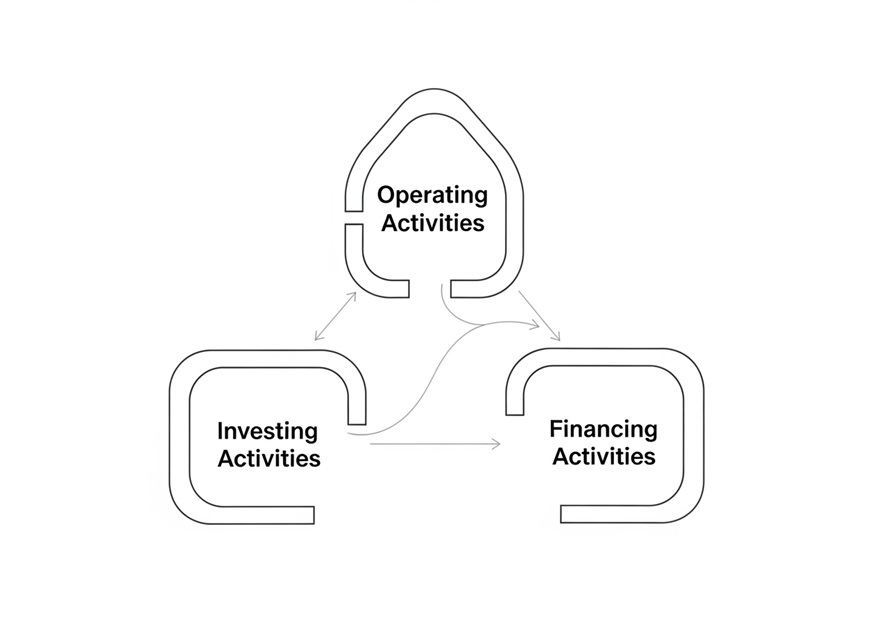

To truly master your business’s financial future, we must first understand the building blocks of a cash flow statement. Whether historical or projected, this document categorizes all cash movements into three main activities: operating, investing, and financing. These categories provide a structured view of where your cash comes from and where it goes, offering a clear picture of your financial situation.

Cash from Operating Activities (CFO)

This section reflects the cash your core business operations generate – the day-to-day activities that produce your revenue. It’s the most crucial indicator of a business’s ability to create money from its primary activities.

Key Inflows:

- Sales Revenue: Cash received directly from customers for goods or services.

- Customer Payments: Collections from accounts receivable.

- Interest Income: Cash received from interest on loans or investments.

Key Outflows:

- Supplier Payments: Cash paid for inventory and other purchases.

- Payroll: Wages and salaries paid to employees.

- Rent & Utilities: Payments for office space, electricity, water, etc.

- Operating Expenses: Other day-to-day costs like marketing, administrative fees, and general overhead.

Understanding your CFO helps you assess how well your business manages its cash position. It shows how effectively you generate cash to pay debts and cover operating expenses.

Cash from Investing Activities (CFI)

This section details the cash flows related to purchasing and selling long-term assets, such as property, plant, and equipment, and investments in other businesses. These activities are often strategic and aimed at future growth or efficiency.

Key Inflows:

- Sale of Property, Plant, and Equipment (PP&E): Cash received from selling assets no longer needed.

- Sale of Securities: Cash from selling investments in other companies.

Key Outflows:

- Purchase of PP&E: Cash spent acquiring new machinery, buildings, or land.

- Buying Securities: Cash is used to invest in other businesses or financial instruments.

Analyzing CFI helps us understand a business’s investment strategy and commitment to long-term growth.

Cash from Financing Activities (CFF)

This final section focuses on cash flows between the business and its owners, lenders, and investors. It reveals how a company raises capital and how it repays its debt.

Key Inflows:

- Bank Loans: Cash received from borrowing money.

- Investor Capital: Cash from issuing new stock or equity.

Key Outflows:

- Loan Repayments: Principal payments made on debt.

- Owner’s Drawings: Cash withdrawn by the business owner.

- Dividends: Cash paid out to shareholders.

CFF provides insight into how a company funds its operations and growth and manages its capital structure.

Creating Your Forecast: A Step-by-Step Guide

Developing a 12-month cash flow statement is a proactive exercise that transforms financial data into actionable insights. It’s about looking forward, anticipating money movements, and preparing for what lies ahead. A cash flow projection is an essential document for determining how much working capital an organization needs to maintain or build to manage the low cash points in the year.

Step 1: Establish Your Opening Balance

Every cash flow statement begins with your starting point: the cash you have on hand.

- Starting Cash: This is the actual cash balance in your bank accounts at the beginning of the first month of your 12-month projection.

- First Month Calculation: For subsequent months, the opening balance will be the previous month’s closing balance. This continuous flow is critical for an accurate projection.

Step 2: Project Your Cash Inflows

This is where we estimate all the money expected to come into your business over the next 12 months. We try to be as realistic as possible, considering historical data, market trends, and upcoming projects.

- Sales Forecasts: Your primary source of cash. Base this on past sales, marketing plans, and anticipated customer demand.

- Accounts Receivable: Estimate when you expect to collect payments from credit sales. Revenue recognition doesn’t always align with cash receipts.

- Loan Proceeds: Any new loans you anticipate securing.

- Asset Sales: Cash from selling old equipment or other assets.

- Seasonal Trends: Account for periods of high and low sales. For example, a retail business might project higher inflows in Q4 due to holidays.

- Other Income: Interest, grants, tax refunds, or other one-off cash injections.

When forecasting estimated figures, consider all forms of income and when they may occur. Look at previous years, identify seasonal trends, and account for regular sources of revenue.

Step 3: Estimate Your Cash Outflows

Next, we project all the money expected to leave your business, including both recurring and one-time expenses.

- Fixed Costs: Expenses that remain relatively constant, like rent, insurance premiums, and salaries.

- Variable Costs: Expenses fluctuate with sales volume, such as raw materials or commissions.

- Inventory Purchases: Cash spent on acquiring goods for sale.

- Taxes: Estimated payments for income tax, sales tax, payroll taxes, etc.

- Insurance Premiums: Annual or semi-annual payments can significantly impact cash in certain months.

- Capital Expenditures: Planned purchases of new equipment, vehicles, or property.

- Loan Payments: Both principal and interest payments on outstanding debts.

- Owner’s Draws/Dividends: Any planned distributions to owners or shareholders.

When forecasting estimated figures, consider all costs needed to run the business and when they will be paid. Forecast cash outgoings by looking at previous years, identifying seasonal trends, and accounting for significant costs. It’s easy to show a monthly profit on a spreadsheet, but go belly up from lack of cash if you can’t pay your bills on time.

Step 4: Calculate Net Cash Flow and Closing Balance

With your inflows and outflows projected, you can now calculate your net cash flow for each month and your rolling closing balance.

- Monthly Cash Balance: Subtract total estimated outflows from total estimated inflows for each month.

- Cumulative Cash Flow: Add the monthly net cash flow to the previous month’s closing balance to get the current month’s closing balance.

- Identifying Surpluses: Months with positive net cash flow indicate periods where you have excess cash.

- Identifying Deficits: Months with negative net cash flow signal potential cash shortages. The 12-month projection truly shines here, allowing you to proactively address these issues.

A projected cash flow statement evaluates cash inflows and outflows to determine when, how much, and for how long cash deficits or surpluses will exist for a farm business during an upcoming time period. This clearly identifies when loan funds will be needed and when the lender can expect to be repaid.

For detailed guidance and templates to assist with your financial planning, especially for anticipating working capital needs and planning for upcoming expenses, consider exploring resources like the Spitz CPA 12-month cash flow planning guide.

The Spitz CPA Approach to Advanced 12-Month Cash Flow Analysis

Moving beyond simply creating the statement, the real power lies in its analysis. A 12-month cash flow statement is not just a report; it’s a dynamic tool for working capital management, strategic decisions, and demonstrating financial acumen to lenders and investors.

Cash vs. Profit: Understanding the Critical Difference

One of the most common misconceptions in business is equating profit with cash. While related, they are distinct concepts; misunderstanding this difference can lead to severe financial problems.

The Key Distinction:

- Profit (from a Profit & Loss Statement): Accrual accounting calculates revenue when earned and expenses when incurred, regardless of when cash changes hands. It includes non-cash items like depreciation.

- Cash (from a Cash Flow Statement): Tracks the actual movement of money into and out of your bank account. It doesn’t care about when a sale was made, only when the cash was received.

Here’s a simple comparison:

Feature Cash Flow Statement Profit & Loss Statement (Income Statement) Purpose: Shows actual cash movements and liquidity. Shows profitability over a period (revenue vs. expenses). Accounting Method: Cash basis (focuses on cash in/out). Accrual basis (focuses on when revenue/expenses are earned/incurred). Key Metrics: Net cash flow, operating cash flow, and ending cash balance. Net income (profit/loss), gross profit. Non-Cash Items Excludes non-cash expenses (e.g., depreciation, amortization). Includes non-cash expenses. Timing Records money when it is received or paid. Records revenue when earned, expenses when incurred. Example: Records cash when a customer pays an invoice. Revenue is recorded when an invoice is issued, even if it has not been paid. As the statistics show, it’s easy to show a monthly profit on a spreadsheet but go belly up from lack of cash if you can’t pay your bills on time. A business can be profitable on paper but still run out of cash if its customers pay slowly or have significant, immediate expenses. Conversely, a company might show a loss but have substantial cash reserves if it sells assets or receives significant loan proceeds.

Choosing Your Method: Direct vs. Indirect for a Spitz CPA 12-Month Cash Flow View

Businesses generally prepare the operating activities section of a cash flow statement using one of two methods: the direct method or the indirect method. When applied correctly, both methods should yield the same net cash flow from operating activities, but they present the information differently.

- Direct Method Explained: This method directly lists the major classes of gross cash receipts and gross cash payments. It’s like a checkbook register, showing exactly where cash came from (cash from customers, interest received) and where it went (money paid to suppliers, employees, for interest, for taxes).

- Pros: Provides a clear, easy-to-understand picture of cash transactions, useful for operational decision-making.

- Cons: Can be more time-consuming to prepare as it requires tracking individual cash transactions.

- Use Cases: These are often preferred by smaller businesses or for internal management, as they offer a detailed view of cash sources and uses.

- Indirect Method Explained: This method starts with net income (from the income statement) and adjusts it for non-cash items (like depreciation and amortization) and changes in working capital (like accounts receivable, accounts payable, and inventory). It essentially reconciles net income to net cash flow from operating activities.

- Pros: It is simpler and less time-consuming to prepare, as it uses figures readily available from the income statement and balance sheet.

- Cons: Can be less intuitive for non-accountants to understand the actual cash movements.

- Use Cases: Widely used by larger companies and for external reporting due to its efficiency in preparation.

While both are valid, the direct method often offers a more intuitive “Spitz CPA 12-Month Cash Flow View” for business owners looking to manage their finances proactively, as it directly illustrates the cash inflows and outflows tied to operations.

From Data to Decisions: Using Your Spitz CPA 12-Month Cash Flow Statement Strategically

Once your 12-month cash flow statement is complete, it becomes a powerful strategic tool.

- Identifying Trends: Spot recurring patterns, seasonal fluctuations, and consistent surplus or deficit periods. This allows for proactive planning rather than reactive problem-solving.

- Managing Working Capital: Use the projections to optimize your working capital. You might plan for early debt repayment or short-term investments if you anticipate a cash surplus. If a deficit looms, you can explore options like extending payment terms with suppliers or accelerating customer collections.

- Planning for Growth: A healthy cash flow enables growth. Use your projections to determine if you have the cash to fund new projects, expand operations, or hire more staff.

- Securing Financing: Lenders and investors scrutinize cash flow statements. A well-prepared 12-month projection demonstrates your financial literacy and ability to repay loans, significantly improving your chances of securing funding. The projected cash flow statement clearly identifies when loan funds will be needed and when the lender can expect to be repaid.

- Making Investment Decisions: Understand your capacity to invest in new assets or technologies without jeopardizing daily operations.

Regularly checking the cash flow statement can spot potential problems early and make informed decisions to keep our business healthy and growing.

Overcoming Common Cash Flow Problems

Cash flow problems are a common cause of small business failure. Businesses will inevitably face challenges even with a carefully prepared 12-month cash flow statement. The key is to anticipate these issues and have strategies to address them.

Managing Seasonality and Fluctuating Revenue

Many businesses experience predictable revenue peaks and troughs throughout the year. Ignoring these seasonal patterns is a recipe for cash flow disaster.

- Anticipating Slow Periods: Your 12-month cash flow statement will highlight these leaner months, allowing you to plan for them.

- Building Cash Reserves: During high-revenue periods, consciously set aside cash to cover expenses during slower times. This acts as a buffer.

- Diversifying Income Streams: Explore ways to generate revenue outside your peak season. For example, a landscaping company might offer snow removal services in winter.

- Adjusting Expenses: Consider flexible staffing or reducing discretionary spending during anticipated downturns.

Failing to plan for seasonal fluctuations can result in cash flow imbalances during slower periods. Regularly reviewing a cash flow statement can help entrepreneurs avoid business failure.

Tackling Accounts Receivable and Payable

The timing of money coming in (receivables) and money going out (payables) is critical for cash flow.

- Invoice Management: Send invoices promptly and ensure they are clear and accurate. Consider offering incentives for early payment.

- Collection Strategies: Don’t let overdue invoices pile up. Implement a systematic follow-up process for late payments.

- Negotiating Supplier Terms: Work with your suppliers to secure favorable payment terms. Can you extend payment deadlines without incurring penalties?

- Payment Cycles: Align your payment cycles with your cash inflows as much as possible. If you know you receive large payments at the end of the month, try to schedule your principal outgoing payments around that time.

Ignoring accounts receivable aging and mismanaging accounts payable are common cash flow mistakes.

The Importance of Regular Review and Updates

A 12-month cash flow statement is not a static document; it’s a living tool that needs constant attention.

- Monitoring Performance: Regularly compare your actual cash inflows and outflows against your projections (monthly is ideal).

- Variance Analysis: Identify significant differences between your projected and actual figures. What caused these variances? Was it higher-than-expected sales, an unforeseen expense, or delayed customer payments?

- Adjusting Forecasts: Update your remaining months’ projections based on your variance analysis and any new information (e.g., a new contract, an unexpected repair). Cash flow is a fluctuating variable, and forecasts are based on estimates. Regular updates are necessary to keep the forecast accurate and reflect current business conditions.

- Monthly Review, Quarterly Adjustments: While a monthly review keeps you on track, a deeper quarterly dive allows for more strategic adjustments to your longer-term forecast.

Reviewing the company’s cash flow statement can help entrepreneurs avoid this fate. New and established business owners can use a cash flow projection to anticipate working capital needs and plan for upcoming expenses.

Frequently Asked Questions about 12-Month Cash Flow Statements.

How often should I update my cash flow forecast?

For a 12-month cash flow statement, monthly updates are considered best practice. Cash flow is a dynamic element of your business, constantly influenced by sales, expenses, and unexpected events. Updating monthly allows you to:

- Track deviations: Quickly identify when actual cash flows differ from your projections.

- Make timely adjustments: Re-forecast the remaining months based on new information, ensuring your plan remains relevant.

- Respond to trigger events: Any significant business change (e.g., a new large client, a major equipment breakdown, a shift in market conditions) should prompt an immediate review and update, regardless of the monthly schedule.

The goal is to maintain an accurate and forward-looking view of your liquidity, enabling proactive decision-making.

What is the biggest mistake businesses make with cash flow?

While there are many pitfalls, one of the biggest mistakes businesses make is ignoring financial projections and operating without sufficient cash reserves. This often manifests as:

- Overestimating revenue: Being overly optimistic about sales without considering potential delays in payment or market downturns.

- Underestimating expenses: Failing to account for all costs, particularly variable expenses, seasonal spikes, or unexpected outlays.

- Lack of contingency planning: Not having a buffer of liquid assets to cover emergencies or sustain operations during lean periods.

These mistakes can lead to a business being “cash poor,” even if it’s profitable on paper. This ultimately jeopardizes its ability to pay bills, invest in growth, or even survive. Cash flow problems are a common cause of small business failure.

Can a cash flow forecast help me get a business loan?

A well-prepared 12-month cash flow forecast is often a critical document when seeking a business loan. Lenders want assurance that you can repay the money you borrow. Your cash flow forecast demonstrates this by:

- Demonstrating repayment ability: It clearly shows the projected cash inflows that will be available to cover loan principal and interest payments.

- Justifying the loan amount: It helps you articulate exactly how much funding you need and for what purpose, showing how the loan will bridge specific cash deficits or fund growth initiatives.

- Enhancing financial credibility: Providing a detailed, realistic, and regularly updated cash flow projection signals lenders that you are financially astute and have a firm grasp of your business’s economic realities.

The projected cash flow statement clearly identifies when loan funds will be needed and when the lender can expect to be repaid, making it an indispensable tool for securing financing.

Conclusion: Taking Control of Your Financial Future

The 12-month cash flow statement is far more than just another financial report; it is the strategic compass that guides your business through the complexities of the market. Understanding its components, carefully forecasting your inflows and outflows, and regularly reviewing your projections can give you unparalleled insight into your financial health.

This proactive approach to financial management empowers business owners to:

- Anticipate and mitigate risks: Spot potential cash shortages before they become critical.

- Optimize working capital: Make informed decisions about managing your day-to-day finances.

- Plan for strategic growth: Confidently invest in new opportunities when cash is available.

- Build financial credibility: Secure the funding necessary for expansion and stability.

In a business world where cash flow problems are a common cause of failure, mastering your 12-month cash flow statement is not just a best practice—it’s a necessity for long-term stability and strategic growth. Take control of your financial future today, and open up the full potential of your business.