Why Is Home Insurance in Miami So Expensive?

Miami homeowners know the struggle: finding affordable home insurance is a constant battle. Premiums here are among the highest in the nation, and we understand that this can be frustrating and confusing.

We know you want to protect your biggest asset without breaking the bank, so we’ve put together this comprehensive guide.

We will explore why homeowners’ insurance in Miami is so expensive. We’ll also explain how your home’s age and location affect your rates. Most importantly, we will share practical steps you can take to find more affordable coverage. For a deeper dive into the specifics, consult our Miami home owners insurance guide.

Our goal is to help you understand your policy options. We want to empower you to make informed decisions and secure the best possible rates for your Miami home.

Miami’s allure is undeniable – sun-drenched beaches, vibrant culture, and a busy metropolitan atmosphere. However, this tropical paradise has a significant financial caveat for homeowners: exceptionally high insurance premiums. We find that the cost of protecting a home in Miami far exceeds national averages, making it one of the most expensive cities in the U.S. for homeowners’ insurance.

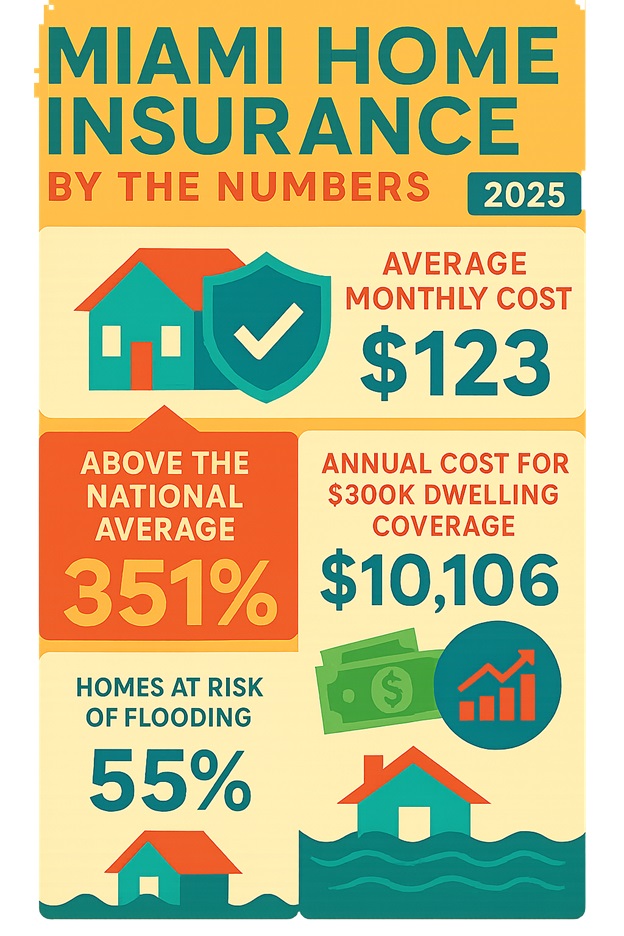

Consider these striking figures: the average homeowners’ policy costs around $123 monthly in Miami, which might seem manageable initially. However, in the broader picture, Miami homeowners can expect to pay an average of 351 percent more than the national average for a home policy. For a typical policy with $300,000 in dwelling coverage, the average annual cost of home insurance in Miami can soar to $10,106. This stark difference highlights the unique challenges property owners face in our region.

The primary drivers behind these lift costs are deeply rooted in Miami’s geography and climate. Situated in a hurricane-prone zone, our city is constantly exposed to the risks of powerful winds, torrential rains, and devastating storm surges. The sheer volume of properties at risk is staggering; USA Today reported that Miami had the most homes of all metropolitan areas in the United States at risk of destruction from storm surge flooding, with almost 800,000 properties identified as vulnerable. Beyond hurricanes, Miami’s low elevation makes it highly susceptible to flooding. Data from Risk Factor indicates that 55 percent of all properties in Miami are at risk of being severely affected by a flood over the next 30 years.

These environmental realities contribute directly to what has been widely termed the “Florida insurance crisis,” a complex issue that has left many homeowners struggling to find affordable and comprehensive coverage.

Understanding the Florida Insurance Crisis

The Florida insurance crisis is a multi-faceted problem beyond just the immediate threat of natural disasters. While frequent storms, particularly hurricanes, constitute a significant factor, the market has been severely destabilized by a combination of high litigation costs, rampant fraudulent claims, and subsequent insurer instability.

According to the Insurance Information Institute (III), Florida homeowner insurers faced cumulative net underwriting losses exceeding $1 billion in 2020 and 2021 alone. In 2023, the losses continued, albeit at a reduced rate, with a $190.8 million underwriting cumulative loss. The disproportionate number of lawsuits is a significant contributor to these financial woes. The Florida governor’s office has pointed out that Florida is the site of an astounding 79% of all homeowners’ insurance lawsuits over claims filed nationally, despite Florida’s insurers receiving only 9% of all U.S. homeowners’ insurance claims. This disparity is often fueled by phony roofing claims and aggressive legal tactics, which drive up costs for insurers and, ultimately, for policyholders.

The financial strain from these factors has led to many insurance companies either leaving the state or becoming insolvent, further limiting options for homeowners. This reduced competition exacerbates the problem, pushing premiums even higher for the remaining insurers.

In response to this crisis, legislative reforms were passed in 2022 and 2023 to curb legal system abuse and claim fraud. While the full impact of these reforms is still unfolding, there is some cautious optimism. As of the summer of 2024, the Office of Insurance Regulation (OIR) has approved eight new property insurers to enter the Florida market, signaling a potential, albeit slow, stabilization. Sean Kevelighan of the Insurance Information Institute noted, “Property insurers want to do business in a state like Florida, which is growing, and there is now some hope that this could eventually happen more and more.” However, continued vigilance and effective implementation of reforms are crucial to ensure a sustainable market for Miami homeowners.

Key Factors Influencing Your Miami Homeowners’ Insurance Premium

Understanding what drives your individual premium is crucial for finding ways to save. While the overall market conditions in Florida play a significant role, several specific home characteristics and your personal profile directly influence the cost of your Miami homeowners’ insurance.

Here are the key factors we consider:

- Home Age and Construction Materials: Older homes often have higher insurance costs. This is because they may have outdated building codes, plumbing, and electrical systems, making them more susceptible to damage and more expensive to repair. For instance, our data shows that a home built in 2020 might pay an average of $1,612 for State Farm insurance, while a house built in 1959 could see premiums as high as $5,596. The materials used in your home’s construction also matter; properties built with resilient materials may qualify for lower rates.

- Roof Condition and Age: The roof is your home’s first defense against Florida’s harsh weather. An older roof, or one in poor condition, signals a higher risk to insurers. A new, hurricane-resistant roof can significantly reduce your premiums.

- Location by ZIP Code: Even within Miami, insurance rates can vary considerably from one neighborhood to another. This is often due to differing flood zone designations, proximity to the coast, and local crime rates. For example, homeowners’ policies in the 32250 ZIP code typically cost just $1,339 per year, $144 less than the Miami average. Conversely, with an annual average premium of $1,559, the 32208 ZIP code tends to be the costliest in Miami for homeowners’ coverage.

- Proximity to Coast: Homes closer to the coastline are inherently at higher risk for wind and storm surge damage, leading to higher premiums.

- Your Claims History: A history of previous insurance claims, particularly frequent or significant, can flag you as a higher risk to insurers, leading to increased premiums.

- Credit Score Impact: In Florida, insurers are permitted to use your credit rating to determine your home insurance rate. A homeowner with a poor credit rating typically pays an average of 5 percent more than a homeowner with good credit for the same policy in Miami. Statistical analysis suggests a correlation between credit scores and the likelihood of filing claims.

By understanding how these factors influence your premium, we can identify areas where you can reduce your costs.

How to Find More Affordable Miami Homeowners Insurance Rates

Given the high cost of homeowners’ insurance in Miami, actively seeking ways to reduce your premiums is not just advisable—it’s essential. We’ve found that homeowners can often find more affordable rates with a strategic approach without compromising on crucial coverage.

One of the most impactful steps is to shop around and carefully compare quotes from multiple insurance providers. The market is dynamic, and rates can vary significantly between companies for the same coverage. This is where the expertise of independent insurance agents becomes invaluable. Unlike captive agents who work for a single company, independent agents work with numerous insurers. This allows us to gather a wide range of quotes and help you find the best combination of price and coverage custom to your specific needs. For more detailed information on navigating the market, our comprehensive Miami home owners insurance guide offers further insights.

Another effective strategy involves adjusting your policy’s deductible. A deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in for a claim. Generally, choosing a higher deductible will result in a lower annual premium. For instance, a $500 deductible results in an average annual home insurance rate of $1,431 in Miami. However, if you increase your deductible to $5,000, your average yearly rate could drop significantly to $1,126. It’s crucial, however, to select a deductible amount you can comfortably afford in case of a claim.

Here’s a breakdown of how increasing your deductible can lead to average annual premium savings:

Deductible Amount Average Annual Premium in Miami Potential Annual Savings (vs. $500 deductible) $500 $1,431 N/A $1,000 $1,317 $114 $2,000 $1,174 $257 $5,000 $1,126 $305 (Note: These figures are averages and actual savings may vary based on individual circumstances and insurer.)

The Power of Discounts and Home Improvements

Beyond shopping around and adjusting deductibles, proactive measures to improve your home’s resilience and leverage available discounts can lead to substantial savings on your Miami homeowners’ insurance. Insurers reward homeowners who mitigate risks, particularly those related to Florida’s prevalent natural disasters.

Here are some standard discounts and home improvements to consider:

- Wind Mitigation Inspection: This is perhaps one of the most significant ways to save in Florida. A certified wind mitigation inspection assesses your home’s ability to withstand high winds. Features like roof-to-wall attachments, roof shape, secondary water barriers, and opening protection (e.g., impact windows or hurricane shutters) can qualify you for considerable discounts. We strongly recommend getting this inspection if you haven’t already done so.

- Impact Windows and Hurricane Shutters: Investing in these protective measures improves your family’s safety during a storm and signals to insurers that your home is less likely to suffer severe wind damage, leading to lower premiums.

- Security Systems and Fire Alarms: Homes equipped with monitored burglar alarms, smoke detectors, and fire suppression systems are generally less risky. Insurers often offer discounts for these protective devices.

- Bundling Home and Auto Policies: Many insurance providers offer multi-policy discounts when you purchase your homeowners and auto insurance from the same company. In Miami, bundling policies can lead to average annual savings of 6%, making it a straightforward way to reduce overall insurance costs.

- New Home Credits: If your home is newly built, it will likely incorporate modern building codes and materials, which can result in lower premiums.

- Claim-Free History: Maintaining a history without recent claims can also contribute to lower rates, demonstrating a lower risk profile to insurers.

By combining these strategies—diligent comparison shopping, strategic deductible adjustments, and proactive home improvements—we believe Miami homeowners can significantly reduce their insurance burden.

Decoding Your Homeowners Insurance Policy

Understanding the components of your homeowners’ insurance policy is fundamental to ensuring you have adequate protection. A standard homeowners insurance policy, most commonly an HO-3 in Florida, is a comprehensive package designed to protect your dwelling, belongings, and liability.

Here’s a breakdown of the typical coverage types included:

- Dwelling Coverage (Coverage A): This is the core of your policy, covering the physical structure of your home, including the roof, walls, foundation, and attached structures like a garage or porch. The amount of dwelling coverage should ideally reflect the cost to rebuild your home from the ground up, not its market value. For instance, in Miami, carrying $200K dwelling coverage costs an average of $1,045 per year, while increasing that coverage to $400K costs an average of $2,058 annually. These figures illustrate how the level of coverage directly impacts your premium.

- Other Structures Coverage (Coverage B): This covers structures on your property that are not attached to your main home, such as detached garages, sheds, fences, and gazebos. It typically provides coverage for about 10% of your dwelling coverage.

- Personal Property Coverage (Coverage C): This protects your personal belongings, including furniture, clothing, electronics, and other possessions, whether they are inside your home or temporarily elsewhere in the world. It’s important to note that certain high-value items like jewelry, art, or firearms may have sub-limits and might require additional coverage (an endorsement or “floater”) to be fully protected.

- Loss of Use / Additional Living Expenses (Coverage D): If your home becomes uninhabitable due to a covered peril (like a fire or severe storm damage), this coverage helps pay for your temporary living expenses, such as hotel stays, restaurant meals, and other increased costs you incur while your home is being repaired or rebuilt.

- Personal Liability Coverage (Coverage E): This is crucial protection for you and your family. It covers legal expenses and damages if you are found legally responsible for bodily injury or property damage to someone else, whether the incident occurs on your property or elsewhere. This could include a guest slipping and falling in your home or your child accidentally breaking a neighbor’s window.

- Medical Payments to Others (Coverage F): This provides limited coverage for medical expenses for people injured on your property, regardless of who is at fault. It’s designed for smaller medical bills and aims to prevent potential lawsuits.

Navigating Special Coverage for Miami Homeowners Insurance

While a standard HO-3 policy provides broad protection, Miami homeowners face unique risks that often require specialized coverage options. We strongly advise understanding these additional protections, as they are critical for comprehensive financial security in our region.

- Hurricane Deductibles: Unlike standard deductibles, hurricane deductibles in Florida are typically a separate, percentage-based deductible (e.g., 2%, 5%, or 10%) of your dwelling coverage. This deductible applies specifically to damage caused by named hurricanes and is usually triggered only once per hurricane season. Understanding this is crucial, as it can represent a significant out-of-pocket expense if your home sustains hurricane damage.

- Windstorm Insurance: In some cases, particularly in coastal areas, windstorm coverage might be excluded from a standard homeowners policy or provided by a separate wind-only policy. Given Miami’s exposure to hurricanes and tropical storms, ensuring robust windstorm coverage is non-negotiable.

- Flood Insurance Necessity: This is perhaps the most critical additional coverage for Miami homeowners. Standard homeowners’ insurance policies do not cover flood damage. With 55 percent of all properties in Miami at risk of severe flooding over the next 30 years, flood insurance is not just recommended; it’s often essential. Flood insurance can be obtained through the National Flood Insurance Program (NFIP), managed by FEMA, or from private insurance companies. If you have a mortgage and your home is in a designated flood zone, your lender will likely require it. The financial risk of not having it is immense, even if unnecessary.

- Citizens Property Insurance Corporation: For homeowners who struggle to secure coverage in the private market, Citizens Property Insurance Corporation serves as Florida’s state-backed “insurer of last resort.” While it can provide a necessary safety net, it’s typically more expensive. It has specific eligibility requirements, often requiring you to demonstrate that you couldn’t obtain coverage from a private insurer.

By carefully assessing your home’s specific risks and ensuring you have these specialized coverages, you can build a resilient insurance portfolio for your Miami property.

Frequently Asked Questions about Miami Home Insurance

We frequently encounter common questions from Miami homeowners navigating the complexities of insurance. Here, we address some of the most pressing concerns to provide clarity and guidance.

Is homeowners’ insurance legally required in Miami?

In Florida, homeowners’ insurance is not legally mandated by state law. However, if you have a mortgage on your home, your lender will almost certainly require you to carry homeowners’ insurance as a loan condition. This requirement protects their financial interest in your property. Lenders typically require enough coverage to at least cover the outstanding balance of your mortgage. They may also require you to maintain an escrow account, where a portion of your monthly mortgage payment goes towards your insurance premiums and property taxes.

Even if you own your home outright and are not legally required to have insurance, going without it is a significant financial risk. Your home is likely your most valuable asset. Without insurance, you would be solely responsible for the cost of repairs or rebuilding after a fire, hurricane, or other covered peril. Furthermore, you would be personally liable for any injuries sustained by guests on your property. We strongly advise all homeowners to maintain adequate coverage, regardless of legal requirements.

What is a hurricane deductible, and how does it work?

A hurricane deductible is unique to homeowners’ insurance policies in hurricane-prone states like Florida. Unlike your standard “all other perils” deductible (which applies to damages from events like fire or theft), the hurricane deductible is typically a percentage of your dwelling coverage (Coverage A), rather than a fixed dollar amount. Typical hurricane deductibles range from 2% to 10%.

For example, if your home has $300,000 in dwelling coverage and a 5% hurricane deductible, you would be responsible for the first $15,000 of covered hurricane damage before your insurance policy begins to pay. This deductible usually applies only once per hurricane season, regardless of how many hurricanes impact your property within that season. Understanding this deductible is crucial, as it can represent a substantial out-of-pocket expense during a significant storm event.

How much dwelling coverage do I actually need?

Determining the right amount of dwelling coverage is one of the most important decisions when purchasing homeowners’ insurance. We advise homeowners to ensure their dwelling coverage reflects the replacement cost of their home, not its market value. Market value includes the land, location, and other factors that don’t relate to the cost of rebuilding the physical structure.

The replacement cost is the estimated amount it would take to rebuild your home from the ground up, using similar materials and quality, after a total loss. This figure can be influenced by local construction costs, labor rates, and your home’s unique features. Underinsuring your home can leave you financially vulnerable if a major disaster strikes, forcing you to pay significant out-of-pocket costs to complete repairs or rebuilding.

To help you estimate this crucial figure, we recommend utilizing a reliable Home Insurance Calculator or consulting with a qualified contractor or appraiser in Miami who can provide accurate local rebuilding costs. The dangers of underinsuring are severe; if your dwelling coverage is too low, your insurer may only pay a pro-rata share of your loss, even for partial damages, leaving you with a substantial financial shortfall. It’s always better to be adequately covered than to face unexpected financial burdens during a crisis.